Fund managers pride themselves on being better than their competitors. But is better best? Marketing experts believe better is subjective. The investment industry’s response? “Not here!”

“Here we’ve got dollar signs and decimal points to prove who is better than whom.”

We’re going to challenge this statement. Because when you stop and think about it - investors typically have more than one manager per asset class and those managers complement each other.

Plus, the biggest funds are not the best performers. And the best performers don't get the most in fund flows. Whatever growth metric you look at, head-to-head competition isn't the path to the winner circle. And let's just be clear, a couple basis points of outperformance doesn’t qualify as a strong differentiator. (Even hundreds of basis points of performance don’t qualify.) Performance is not an edge. It might be an outcome of your edge, but the performance itself isn't the differentiator. We have to go a layer deeper.

What’s better than better?

Instead of focusing on results, what if we challenged ourselves to key in on the real drivers for differentiation?

First, let’s look at a few little brands you may have heard of.

Airbnb. They revolutionized the hospitality industry by offering unique travel experiences. Not everyone would agree they’re better or worse than traditional hotels, but we can all agree they’re different and can easily identify how they’re different.

Zappos. They were one of the first well known retailers to offer free shipping and easy returns. They didn’t sell shoes that were better or worse than your local department store, but they provided a very different customer experience.

Trader Joe's. They stand out in the grocery industry by offering unique private-label products and training their employees to create a fun, chill shopping environment. Not everyone probably agrees whether their pasta tastes better or worse than Safeway’s or Costco’s, but I bet we can all feel the difference when we step into the store.

These brands have successfully carved out their niches by focusing on being different. They’ve attracted loyal customers and achieved long-term success in their respective markets.

You too can identify and lean into your edges.

Being better is temporary

New York Times best-selling author, Sally Hogshead, asserts that striving to be “better” keeps you chained to your competitors' way of working. She emphasizes that being better is a temporary advantage that can easily be toppled in a millisecond by someone with a bigger following, or a lower price or better location, a shinier award, a newer technology or a fancier degree. (Or ahem, better performance.) It's not enough. Instead, we should focus on what makes us radically different and fascinating.

If we are trying to compete at a level of, “I'm better than this person or this company or this fund,” we have to compete the same way that they are. It's very hard to stand out when you're doing the same thing as everybody else.

Carving out your niche helps you attract & repel

There’s a marketing strategy called a "category of one" where a company positions itself as the only or most distinct provider of a particular product or service within its industry. In other words, the company aims to create such a unique and compelling brand identity that it effectively eliminates direct competition.

What if you became a category of one?

To achieve this, you need to specialize, carve out a niche, and develop something so distinct that it both attracts and repels. This concept can be applied to individuals, companies, and funds alike. It's about challenging the status quo, leaning into what you stand for and against, and asking yourself if you’re brave enough to attract and repel.

Differentiation is hard

Differentiation is easy to identify when we see it, but putting a framework around it is more challenging.

A study by Bain & Company found that while 80% of execs believed their company's offerings were differentiated, only 10% of customers agreed. The customers didn’t perceive that differentiation. And here’s the important part, a brand is all in the perception. It’s in the minds and hearts and souls of your customers and prospects. The Bain study highlights a fundamental challenge: we often fail to define what truly makes us different.

Marty Neumeier, author and branding pioneer, says that companies often underestimate the level of differentiation required to truly stand out. He talks about the concept of an “accidental brand,” one you stumble upon. You tried something, it worked, but you don't actually know how you did it, so you can't repeat it. That’s not enough. You need to find repeatable differentiators that define your edge.

Identifying Your Differentiators

Often what we believe sets us apart sounds eerily similar to everyone else. Our claimed differentiators mirror others’, which by definition cease to differentiate us.

Advisors see a ton (and we mean, a ton) of presentations every year. If yours looks like everyone else’s… if it says all the same things - a bunch of truisms or how many years experience your people have - it won’t stand out. They’ve seen it all before. It's human nature to want to fit the norm, but to find your true fans, you need to set yourself apart.

Ready to do the work? Let’s be brave together.

1. Ask questions

Get a pen and paper out and write down the answers to these questions.

- What makes you different?

- What do you stand for?

- What aspects of your industry do you like or dislike?

- Why this strategy?

- What do you do that no one else does?

- What do you do differently than your peers (and can you repeat it)?

- What 20% do you do that drives 80% of your results?

- What frustrates you about your space?

2. Fight truisms

UK allocator Dan Mikulskis meets with hundreds of asset managers every year. On episode 5 of Billion Dollar Backstory podcast, he talks about how he’s tired of seeing truisms in manager presentations.

Truisms are statements that have no valid counter-argument. For instance, if you state that your people are your differentiator (“we have great people!”), consider if the opposite could be a valid statement for any organization (“our people suck!”). If the answer is no company would say that, then your differentiator might be a truism.

If the opposite is valid, then you've hit on something. Maybe you say, "we believe that a portfolio should not be more than 15 names." Could someone argue with that? Sure. That’s a valid differentiator.

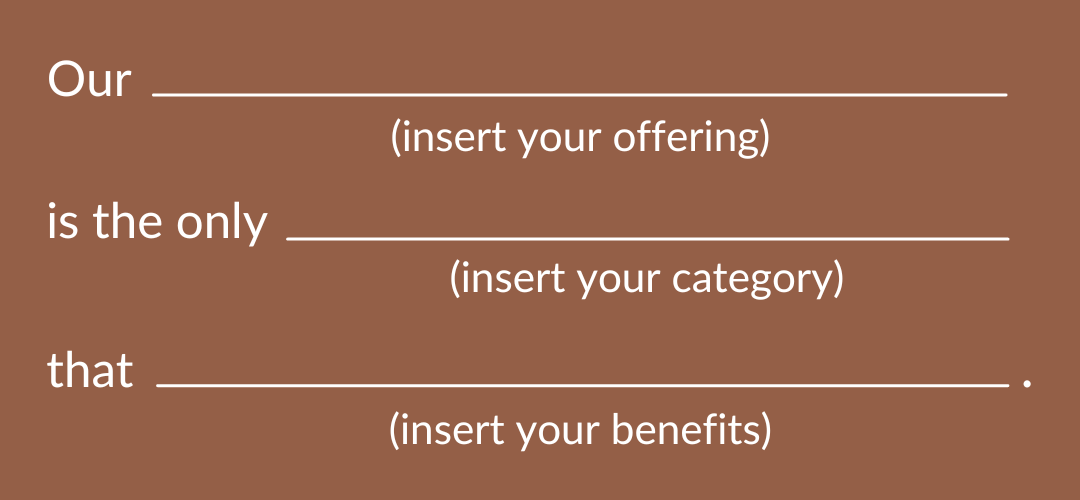

3. Create an onlyness statement

Coming back to Marty Neumeier - his book, "Zag," offers an exercise that revolves around the concept of creating a category of one by crossing unique elements. It’s a mad lib of sorts; try filling it out:

What are the unique elements, maybe things that don't even seem related, that when you cross them, create this onlyness statement?

4. Old Way vs. New Way

Old way vs. new way is a strategy championed by author and keynote speaker Andy Raskin that focuses on how your offering marks a departure from the traditional approach, presenting a new and improved way of doing things. A classic example of this strategy in action is when Salesforce.com disrupted the market with its cloud-based software, declaring it the new way against the old way of traditional software.

In Billion Dollar Backstory Episode 3, $20B Carson Group’s founder, Ron Carson, highlighted old way vs. new way in the investment industry. He took us back to the early days of his career, highlighting how the old way was treating clients as mere numbers with no fiduciary responsibility. The shift to a fiduciary model, where advisors were accountable and transparent, marked the first significant shift in the financial advisory sector.

5. Ask your investors

You can also ask your investors how they are using you. What do they think makes you different? What strategies or funds are you complementing? Oftentimes allocators are trying to balance out exposures or how managers think and what makes their process unique.

6. Check yourself before you wreck yourself

Got some differentiators written down now? Final check. If you can swap out your name with that of a competitor in your statement and it still holds, it’s not differentiated.

Escaping the Zero-Sum Game

The investment industry often views attracting investors as a zero-sum game - for you to win, someone else has to lose. But this is a narrow viewpoint. There isn't just one allocation or one manager in an asset class. Diversification, concentration risk, and business risk all play a part.

Discovering your unique differentiators involves understanding your values, challenging the status quo, and having the courage to stand out.

As you navigate these exercises, remember different is not just better; it's the best.